2020 was a volatile year that saw financial institutions in the consumer and commercial lending space exposed to significant operational risk. This risk was multiplied for the financial institutions that relied on third-party subservicers, as these firms had to consider not only their own risk profile but that of the third parties servicing their portfolio and engaging with their borrowers.

Financial institutions had to manage through a global pandemic that caused high unemployment and a stock market crash, followed by fluctuating rates, new regulations, growing cyber-risk exposure, and historic economic recovery requirements.

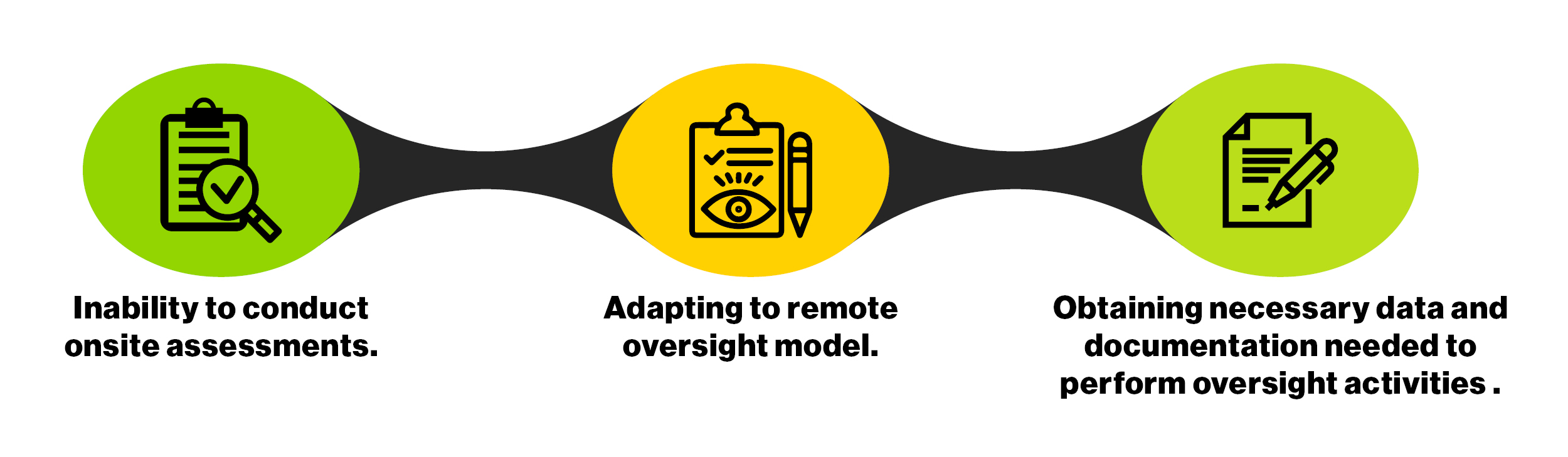

These events brought several challenges to third-party oversight teams, especially maintaining the ability to conduct business in the manner they were accustomed. Many financial institutions struggled with:

While financial institutions may have been inclined to deprioritize third-party oversight in the face of the business disruption observed in 2020, it is vital that financial institutions in 2021 remain vigilant in their oversight responsibilities. With many Americans still economically burdened, cyber threats on the rise, new regulations coming from the Coronavirus Aid, Relief, and Economic Security Act, and new Consumer Financial Protection Bureau leadership, third-party oversight will be a key issue for regulators to focus on in 2021.1

This article explores the key risks facing third-party oversight teams in 2021, and some mitigation strategies to help prepare you to appropriately manage risk in this evolving landscape.

Deutschland

Deutschland India

India Lietuva

Lietuva United Kingdom

United Kingdom Search

Search